The dirty business of asset management is an open secret.

Asset management firms research, buy, and sell marketable securities. Financial planners and wealth management firms allocate investors money to asset management firms. Asset management firms, like BlackRock, grow revenue every year.

Clients' must know more about the dirty business of asset management. Generally speaking, financial advisors have the tools to weed out the bad ones.

Asset management firms offer active and passive solutions. Firms such as Vanguard, and a parts of BlackRock offer passive investments. Their strong asset growth over the last decade made them the new leaders.

We all the know reasons for this. Firms such as Fidelity, PIMCO, and Goldman Sachs offer active investments. Their asset growth has stalled. As of 12/31/2015, global asset management firms AUM equaled $76.7 trillion. US based firms AUM equalled $44 trillion (source: WillsTowersWatson 2016, The World’s 500 Largest Asset Managers report).

The definition of asset management should include venture capital, private equity, and hedge fund firms. To sum up, their profit compared to AUM outshines active asset management firms.

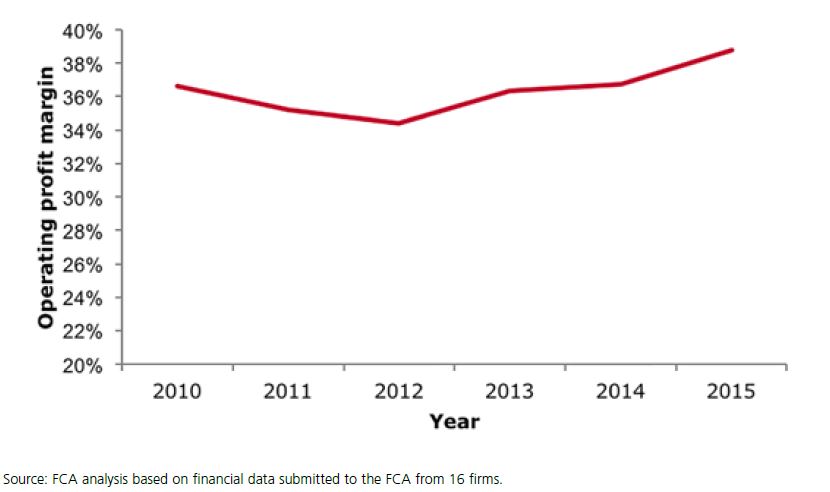

Source: FCA

Source: FCAAn open industry secret of these firms center on lax cost controls. Employees, marketing, and bid/ask spreads cover the majority of expenses. The 'quiet' expenses of transfer agents, custodians, legal, and accounting firms continue to increase.

Employee head counts and bid/ask spreads have narrowed. Servicing costs have become very efficient. Today the costs are the dirty business of this industry. Nonetheless, operating profit margins remain at strong levels.

Mutual funds lend their assets to a short seller. Short seller’s profit assets decline. Mutual fund and asset management firms earn large fees lending out stocks and bonds. Vanguard, DFA and State Street are big users of this fee generation.

Accordingly most reduce fees by a portion of fees earned via lending out their assets. What happens when investors sell a mutual fund in a panic? The mutual fund sells assets to match investor redemptions. The mutual fund needs to 'call back' the stocks and bonds lent out to short sellers. Everyone expects the selling and returning stocks and bonds to happen on time.

However, this does not always happen. During the financial crisis, Money Market funds did not get back their loan bonds. Stock mutual funds had time mismatches leading to a short cash position. Mutual funds pass this cost onto investors.

With this in mind, the dirty business of the asset management industry lies in operational risks. To emphasize, the lending out mutual fund assets adds complexity. As a result, the plumbing of Wall Street complexity defies imagination.

To clarify, the risk centers on liquidity to match buying and selling. Assets with large leverage exposure increases this risk. In normal times, everything runs smoothly. In times of panic or nervousness, the process does not work well. Asset classes with large leverage exposure experience the largest pain which investors pay for.

Wall Street's Achilles heel has always been the operational and leverage side of the business. The dirty business of asset management centers around lending out their assets. Regardless of the fee benefits of lending out assets, mutual funds clearly do not explain this to investors.

Free lunches do not exist on Wall Street.